The following information was taken from the Senate Bill 1 Public Act 98-0599.

Senate Bill 1 passed both chambers of the General Assembly and has been signed into law by the Governor as Public Act 98-0599. The Act affects active Tier 1 members, inactive Tier 1 members and Tier 1 retirees of SERS. The effective date of Public Act 98-0599 is June 1, 2014. Tier 2 members are NOT affected by the Act. The Act does NOT reduce the current monthly benefit amounts of Tier 1 retirees and it does NOT eliminate or reduce COLAs that have already been received by retirees. The ACT does NOT change the COLAs of widow, survivor and disability annuities. The January 2014 COLA is NOT affected by Public Act 98-0599 as it reduces COLAs beginning in January 2015.

DEFINED BENEFIT (DB) CHANGES

Maximum Annual Adjustments (COLAs): The Act does not affect the January 2014 COLA. Beginning January 2015, the 3% COLAs will be applied to the lesser of the actual annuity, or the number of years of a retiree’s service credit multiplied by $1,000 for service not covered by Social Security or $800 for service covered by Social Security (maximum COLA amount). The maximum COLA ($1,000 or $800 per year of service) will be indexed each year by the growth in the Consumer Price Index (CPI).

There is no limit on the number of years of service credit that can be used in the maximum COLA calculation. All optional service credit, including sick leave, qualifying periods and ERI service credit will be included in the calculation. Reciprocal service credit with other retirement systems will not be used in the COLA calculation.

Those with an annuity that is less than their years of service multiplied by the applicable $1,000 or $800 multiplier will receive a 3% COLA compounded each year until the annuity reaches the maximum COLA amount.

COLA CALCULATION EXAMPLE

To calculate the January 2015 COLA amount, for members covered by Social Security, SERS will multiply a retiree’s total years of service credit (including sick leave, qualifying periods, and all other optional service) by $800 and the 3% COLA will be applied. For a member with 30 years of SERS service credit, the 3% COLA would be applied to $24,000 (30 years X $800). The resulting FY 15 COLA would be $720 annually ($24,000 X 3%) or $60 per month. To calculate the FY 15 COLA for members not covered by Social Security, substitute $1,000 for $800 in the above example.

Beginning with the January 2016 COLA, the $800 and $1,000 multipliers will be increased by the CPI. For example, if the CPI is 2% for the year ending September 2015, the January 2016 COLA multipliers will become $816 for years of service credit covered by Social Security and $1,020 for years of service credit not covered by Social Security. The multipliers continue to increase annually at the CPI rate but do not decrease if inflation is negative.

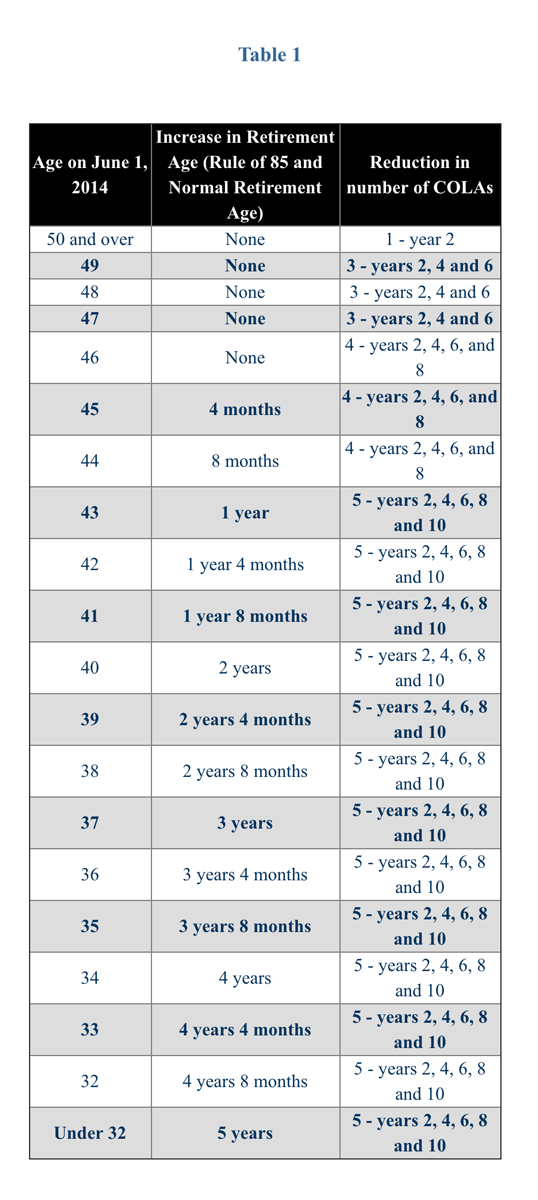

Skipped COLAs: Tier 1 Employees who retire on or after July 1, 2014 will have annual adjustments skipped depending on age as of June 1, 2014: employees age 50 or over, 1 COLA skipped (2nd COLA); employees age 47 to 49 will have 3 COLAs skipped (2nd, 4th, and 6th COLA); employees age 44 to 46 will have 4 COLAs skipped (2nd, 4th, 6th, and 8th COLA); employees age 43 and under, 5 COLAs skipped (2nd, 4th, 6th, 8th, and 10th COLA). Please refer to Table 1 below.

Pensionable Salary Cap: The Act creates an annual pensionable salary cap for Tier 1 members. For each Tier 1 member, this cap is the greatest of the following:

- The Tier 2 salary cap ($110,631 for 2014). This cap is adjusted annually by the lesser of 3% or ½ of the previous year’s CPI

- For a member covered by an individual contract or collective bargaining agreement (CBA) that is in effect prior to June 1, 2014, the member’s salary on the day the contract or CBA expires. A contract cannot be amended or extended to increase the cap

- For a member not covered by an individual contract or CBA (merit comp employees), the annualized salary on June 1, 2014

A member will make employee contributions on compensation up to the applicable annual salary cap and will not make employee contributions on compensation above the cap. Only compensation up to the applicable annual salary cap will be included in the calculation of the member’s Average Final Compensation (AFC) at retirement.

Retirement Age: For Tier 1 employees age 45 or younger on June 1, 2014, the retirement age is increased on a graduated scale. For each year a member is under 46, the retirement age will be increased by 4 months (up to a 5 year increase for members under age 32 on June 1, 2014). The incremental increase in retirement age applies to all formulas and the Rule of 85. Please refer to Table 1 below.

Employee Contributions: Beginning July 1, 2014, all Tier 1 employee contribution rates will decrease by 1%.

Service Credit for Accumulated Sick and Vacation Days – New Hires: Employees who first become SERS members after June 1, 2014, are not allowed to convert accumulated sick and vacation days into service credit at retirement. Current SERS members will still be able to convert these days into service credit at retirement.

OPTIONAL DEFINED CONTRIBUTION (DC) PLAN

Defined Contribution Plan: Beginning July 1, 2015, up to 5% of Tier 1 active members can make an irrevocable election to switch from the DB plan to a DC plan. Employee contributions to the DC plan will be equal to those of the DB plan. Employer contributions to the DC plan will change annually and must be at least 3% but not higher than the employer’s cost of the DB benefits. The employee must participate in the DC plan for at least 5 years to become vested in the employer contributions made to their DC account. When a member opts into the DC plan, benefits previously accrued in the DB plan will be frozen.

FUNDING CHANGES

Funding Schedule: A funding schedule is established that will achieve 100% funding no later than the end of FY 2044. Contributions will be certified using the entry age normal (EAN) actuarial cost method, which spreads costs evenly over an employee’s career and results in level employer contributions.

Supplemental Contributions: The State will contribute (i) $364 million in FY 2019, (ii) $1 billion annually thereafter through 2045 or until the system reaches 100% funding, and (iii) 10% of the annual savings resulting from pension reform beginning in FY 2016 until the system reaches 100% funding. The supplemental contributions will be divided among the State-funded retirement systems based on each system’s proportional share of the State’s total unfunded liabilities.

Funding Guarantee: If the State fails to make a required annual or supplemental contribution, the Act allows SERS to file an action in the Illinois Supreme Court to compel the State to make the required annual or supplemental contribution.

This table was taken from the Senate Bill 1 Public Act 98-0599.